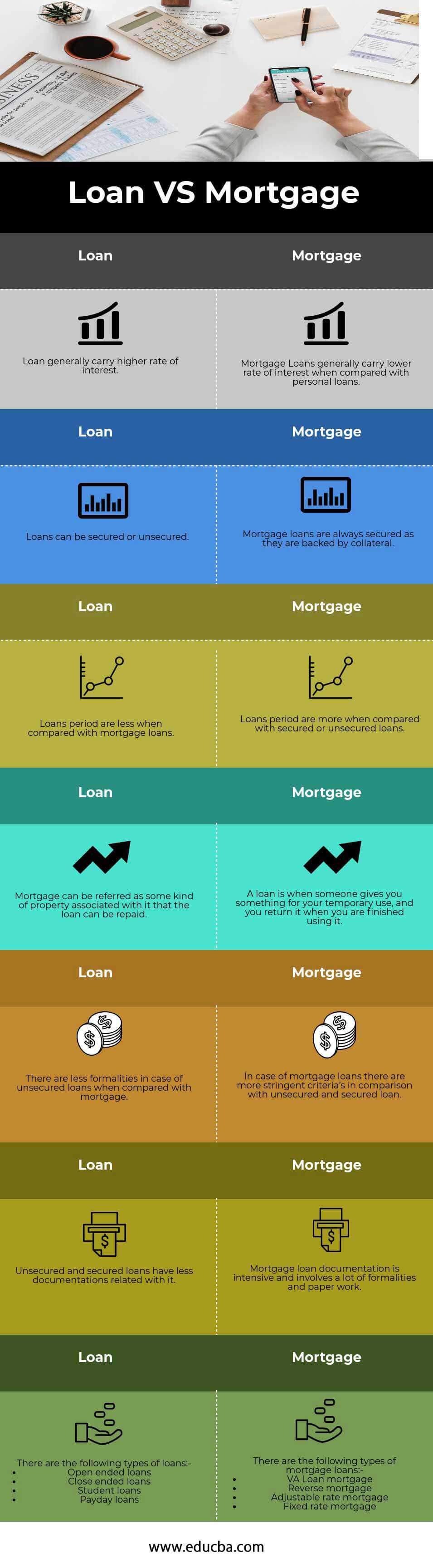

Tips To Help You Out With Your Home Mortgage

Content author-Rask CrossA mortgage is truly a huge milestone in a person's life, whether they are 18 or 80 when they get it. The fact is that knowing the right things before you get started can make the process better. This article has what you need to know, so read it in full.

Before beginning any home buying negotiation, get pre-approved for your home mortgage. That pre-approval will give you a lot better position in terms of the negotiation. It's a sign to the seller that you can afford the house and that the bank is already behind you in terms of the buy. It can make a serious difference.

Knowing your credit score is important before trying to obtain a mortgage. The better your credit history and score, the easier it will be for you to get a mortgage. Examine your credit reports for any errors that might be unnecessarily lowering your score. In reality, to obtain a mortgage, your credit score should be 620 or higher.

Do not go on a spending spree to celebrate the closing. A recheck of your credit at closing is normal, and lenders may think twice if you are going nuts with your credit card. https://elynews.com/2022/03/06/a-g-henry-jr/ buying, as well as any other expensive item or project, needs to wait until your mortgage contract is signed and a done deal.

Try getting pre-approved for a mortgage before you start looking at houses. This will make the closing process a lot easier and you will have an advantage over other buyers who still have to go through the mortgage application process. Besides, being pre-approved will give you an idea of what kind of home you can afford.

Avoid fudging the numbers on your loan application. It is not unusual for people to consider exaggerating their salary and other sources of income to qualify for a larger home loan. Unfortunately, this is considered froud. You can actually be criminally prosecuted, even though it doesn't seem like a big deal.

Pay off your mortgage sooner by scheduling bi-weekly payments instead of monthly payments. You will end up making several extra payments per year and decrease the amount you pay in interest over the life of the loan. This bi-weekly payment can be automatically deducted from your bank account to make it easy and convenient.

Base your anticipated mortgage on what you can actually afford to pay, not solely on what a lender preapproves you for. Some mortgage companies, when pleased with the credit score and history they review, will approve for more than what a party can reasonably afford. Use this for leverage, but don't get into a mortgage that's too big for your budget.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

Choose your mortgage lender many months in advance to your actual home buy. Buying a home is a stressful thing. There are a lot of moving pieces. If you already know who your mortgage lender will be, that's one less thing to worry about once you've found the home of your dreams.

Keep your credit score in good shape by always paying your bills on time. Avoid negative reporting on your score by staying current on all your obligations, even your utility bills. Do take out credit cards at department stores even though you get a discount. You can build a good credit rating by using cards and paying them off every month.

Pay off your mortgage sooner by scheduling bi-weekly payments instead of monthly payments. You will end up making several extra payments per year and decrease the amount you pay in interest over the life of the loan. This bi-weekly payment can be automatically deducted from your bank account to make it easy and convenient.

Put as much as you can toward a down payment. Twenty percent is a typical down payment, but put down more if possible. Why? The more you can pay now, the less you'll owe your lender and the lower your interest rate on the remaining debt will be. It can save you thousands of dollars.

click over here now or twenty year loan is worth investigating if you can manage the payments. With the shorter loan term you get reduced interest rates that allow you to pay it down much quicker. This can save you thousands over the term of your mortgage.

If you are a first time home owner, get the shortest term fixed mortgage possible. The rates are typically lower for 10 and 15 year mortgages, and you will build equity in your home sooner. If you need to sell you home and purchase a larger one, you will have more cash to work with.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

One item of documentation for home mortgage application that is often overlooked is a gift letter. If your relatives have chipped in to help you make your down payment, you may need to document your source of income. This really depends on the type of home mortgage you get. Some require this, and others do not. Play it safe by getting a gift letter from anyone who gives you money to help you buy your home. Have this on file with your other documentation.

Get your credit under control. If you currently have a wallet full of plastic for every occasion, you should downsize. Having too much available credit can harm your loan, even if it is not debt. Close any non-essential accounts. Chose a gas card, a store card, and a single credit card to keep.

Though you may feel a little overwhelmed with financing your home mortgage, you can use the tips you got here to boost your confidence. Most of the stress of home buying is from not fully understanding the process. If you keep the information you got here in mind, you are already ahead of the game.